Executive Summary

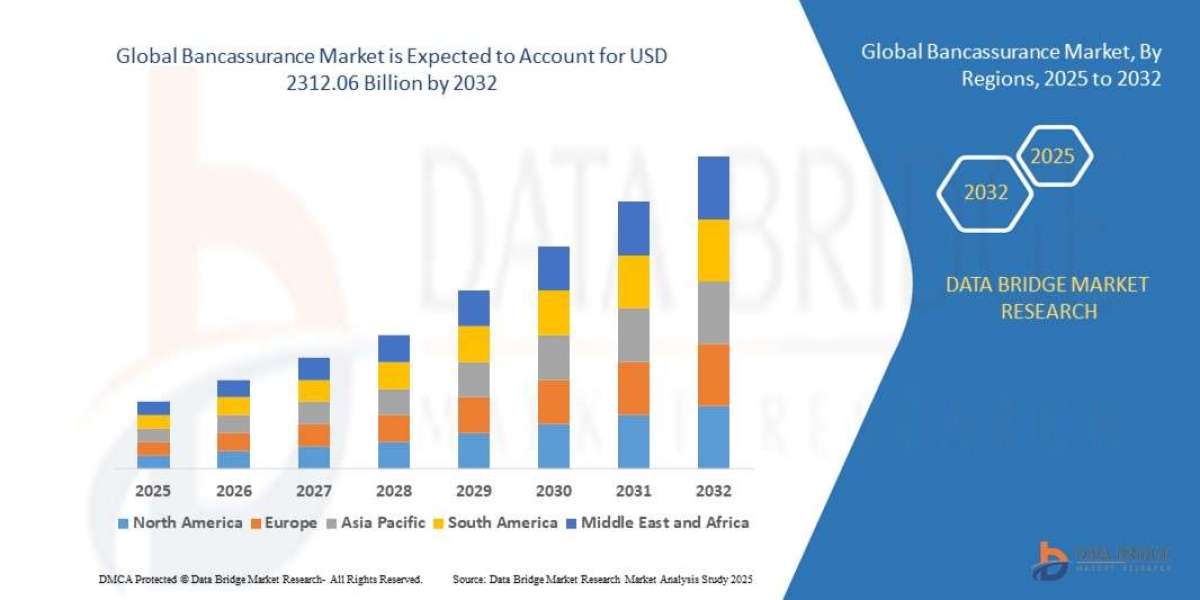

- The global bancassurance market size was valued at USD 1506.54 billion in 2024 and is expected to reach USD 2312.06 billion by 2032, at a CAGR of 5.50% during the forecast period

? Market Overview

Defining Bancassurance and its Core Models

Bancassurance is an arrangement between a bank and an insurance company allowing the insurance company to sell its products to the bank’s client base. This strategy capitalizes on the bank's extensive distribution network, customer trust, and transactional data.

The model is typically categorized into three main partnership structures :

Pure Distributor Model: The bank acts merely as an agent, selling the insurer’s products for a commission. This is the simplest and most common form.

Strategic Alliance Model: A deep, long-term partnership where both entities collaborate on product development, marketing, and shared resources.

Joint Venture (JV) Model: A new, separate legal entity is created, jointly owned and controlled by both the bank and the insurer, sharing risks, rewards, and operational control.

Key Market Segments

By Insurance Type:

Life Bancassurance: Historically dominant (accounting for around 60-63% of the market). Driven by demand for savings, retirement, and long-term protection products, often linked to mortgages or fixed deposits.

Non-Life (P&C) Bancassurance: Includes property, casualty, health, motor, and travel insurance. This segment is accelerating, particularly due to the demand for health and general insurance, and is increasingly integrated into digital channels.

By End-User: The market is dominated by Individual/Retail Customers but the Small and Medium Enterprises (SMEs) and Corporate segments are showing fast growth, demanding tailored group schemes and risk management solutions.

By Distribution Channel: Traditional Bank Branches remain the largest channel, especially for complex or high-value life products. However, Digital Channels (online, mobile apps) are the fastest-growing channels, driven by the shift towards seamless, self-service solutions.

Drivers and Current Dynamics

The market's current momentum is propelled by several key factors:

Banks' Quest for Fee-Based Income: Amidst pressure on traditional Net Interest Margins (NIMs), selling insurance offers a stable, high-margin, non-interest revenue stream for banks.

Customer Trust and Convenience: Customers show a high degree of trust in their banks for financial advice and prefer the one-stop-shop convenience of managing their banking and insurance needs in a single location or app.

Growing Financial Literacy and Wealth: Economic growth, particularly in emerging markets, is increasing the middle-class population, raising financial literacy, and fueling demand for financial security and wealth management products.

Supportive Regulatory Environment: Governments and regulatory bodies, like the IRDAI in India, are introducing mandates and reforms to encourage bancassurance, often as a tool for increasing national insurance penetration and financial inclusion.

? Market Size & Forecast

- The global bancassurance market size was valued at USD 1506.54 billion in 2024 and is expected to reach USD 2312.06 billion by 2032, at a CAGR of 5.50% during the forecast period

For More Information Visit https://www.databridgemarketresearch.com/reports/global-bancassurance-market

? Key Trends & Innovations

The bancassurance model is undergoing a profound digital transformation, moving beyond simple referral systems to deep technological integration.

1. Digital Bancassurance and Embedded Insurance

The most significant trend is the shift to Digital Bancassurance. This involves integrating the insurance purchasing journey directly into the bank's digital platforms (mobile apps, online portals). The emergence of Embedded Insurance is the next frontier, where a relevant insurance product is seamlessly offered at the point of a non-insurance transaction (e.g., offering property insurance during a mortgage application, or travel insurance during a flight booking on a bank's platform). This relies heavily on flexible architecture like APIs (Application Programming Interfaces) to connect bank and insurer systems .

2. Hyper-Personalization via AI and Big Data

Banks possess a wealth of transactional and behavioral data on their customers. By leveraging Artificial Intelligence (AI) and Advanced Data Analytics, banks can move away from generic product pushing toward hyper-personalization. AI models can analyze a customer's life stage, income, credit history, and spending patterns to predict their insurance needs (e.g., life cover needed for a new loan, or health coverage for a new parent) and deliver a tailored, needs-based recommendation in real-time.

3. Open Finance and Open Insurance

Regulatory trends like Open Finance facilitate the secure sharing of financial data between institutions (with customer consent). This enables banks and insurers to create more holistic, customer-centric value propositions. Open Insurance specifically focuses on creating an ecosystem where insurance products are easily consumable across various financial platforms, making bancassurance more efficient and transparent.

4. Focus on Protection and Health Products

Post-pandemic, there is a heightened global awareness of financial vulnerability, driving increased demand for pure protection products (term life) and health & wellness insurance. Bancassurers are responding by developing more comprehensive, modular, and easy-to-understand products in these segments.

? Competitive Landscape

The competitive landscape is a confluence of major global financial groups, regional banking powerhouses, and specialized insurance carriers.

Major Players and Market Strategies

The market is generally characterized by a medium concentration, with major global banking and insurance groups holding substantial market share through joint ventures and exclusive partnerships. Key global players include:

Global Leaders: Allianz, AXA, BNP Paribas Cardif, Banco Santander, Generali, and Prudential. These entities often leverage captive companies or joint ventures for deep integration, especially in European markets.

Regional Powerhouses: Local champions, such as State Bank of India in India or key regional banks in Southeast Asia, dominate their respective domestic markets by utilizing their vast branch networks and deep local trust.

Competitive Strategies

Exclusive Partnerships and Joint Ventures (JVs): Many leading players opt for exclusive, long-term JVs to maximize value capture, streamline operations, and create truly unified product offerings. The commitment required in a JV encourages both parties to invest heavily in the model's success.

Digital Distribution Dominance: The competitive edge is rapidly shifting from the size of the branch network to the quality of the digital user experience. Players are competing on seamless digital onboarding, instant policy issuance, and self-service claims processing via mobile apps.

Product Differentiation: Competitors are moving beyond standard term-life and simple P&C products to offer highly customized solutions for specific customer segments (e.g., high-net-worth individuals, SMEs, or micro-insurance for the financially excluded).

Sales Force Transformation: Success hinges on transforming the bank's traditional front-line staff from transaction processors to competent financial advisors capable of needs-based selling. This requires substantial investment in training, certification, and technology-driven sales tools.

? Regional Insights

Bancassurance adoption and model maturity vary significantly across global regions, reflecting diverse regulatory frameworks and consumer behaviors.

Europe (Matured Market): Historically the heartland of bancassurance, with countries like France, Spain, and Italy showing very high penetration rates (often exceeding 50% for life insurance). Growth is steady, driven by demand for retirement and protection products and the need for banks to optimize their branch networks through digital integration.

Asia-Pacific (Fastest Growth): Projected to grow at the fastest CAGR, driven by low insurance penetration, rising disposable incomes, and the massive, underserved customer bases of large national banks in countries like China, India, and Indonesia. The focus here is on mass-market distribution and leveraging mobile banking for first-time policy buyers.

North America (Growing Adoption): Traditionally a broker-dominated market, bancassurance is gaining traction, particularly as large financial institutions seek to cross-sell wealth management and simple P&C products. The adoption of digital platforms is high, providing strong tailwinds for this channel.

Latin America and Middle East & Africa (Emerging Potential): These regions represent significant untapped potential. Growth is accelerating due to supportive regulations, increasing financial literacy, and the expansion of modern banking infrastructure. The strategy here often involves pioneering new distribution models and focusing on basic protection products.

? Challenges & Risks

Despite the promising outlook, the bancassurance market faces several structural and operational hurdles.

Regulatory Complexity and Compliance: The regulatory landscape is often fragmented, with overlapping rules for banking and insurance across different jurisdictions. Banks must comply with stringent conduct-of-business rules, data privacy laws (like GDPR), and anti-mis-selling mandates, which can significantly increase compliance costs (estimated to account for up to 10% of operational expenses for some providers).

Cultural and Operational Integration: Integrating two fundamentally different organizational cultures—the conservative, compliance-focused bank and the sales-driven insurance company—is notoriously difficult. Misalignment in incentives, IT systems, and product development pipelines often leads to partnership friction and sub-optimal customer experience.

Lack of Specialized Staff Expertise: Bank employees are primarily trained for banking products. Selling insurance requires a different skill set—needs analysis, risk assessment, and long-term financial planning. The difficulty in upskilling or recruiting a dual-skilled sales force can lead to poor quality of advice and potential reputational risk from mis-selling.

Digital Disintermediation: The rise of independent InsurTechs and BigTechs offers customers direct, highly efficient digital channels, potentially eroding the bank’s traditional advantage as the sole 'trusted' channel for financial products.

? Opportunities & Strategic Recommendations

For stakeholders, the market presents immense opportunities, provided they adopt a digitally focused, customer-centric strategic approach.

For Banks (The Distributor)

Transform from Agent to Advisor: Invest heavily in AI-driven training and sales tools to equip relationship managers to conduct credible needs-based selling, especially for complex Life and Wealth products. Shift the focus from selling a product to providing a comprehensive financial plan.

Double Down on Digital Integration: Implement an "Embedded Finance" strategy by integrating insurance APIs directly into mobile and online banking journeys. The goal is seamless, contextual cross-selling (e.g., a one-click insurance add-on for a new credit card or loan).

Target the SME Segment: Develop tailored employee benefits, trade credit, and commercial property insurance packages for the SME customer base, which is underserved and often highly loyal to its primary bank.

For Insurers (The Product Manufacturer)

Co-Create Digital Products: Work with bank partners to design simple, modular insurance products that are "digital-first"—easy to understand, buy, and claim through a mobile app. Prioritize simple P&C and supplementary health products for instant digital uptake.

Invest in Data Sharing Technology: Focus on building robust, secure, and flexible API gateways that allow the bank to leverage customer data for predictive underwriting and personalized offers without compromising data privacy.

Embrace Multi-Partner Models: While exclusivity has benefits, insurers should also explore non-exclusive or broker-like partnerships with smaller, digital-only banks (Neobanks) or Fintech platforms to broaden market reach and test new distribution technologies.

For Investors and Private Equity

Target InsurTech Enablers: Invest in technology companies specializing in Bancassurance-as-a-Service platforms, AI-powered underwriting, and digital compliance solutions that bridge the IT gap between banks and insurers.

Focus on Emerging Markets JVs: Emerging markets offer exponential growth. Target investment in successful Joint Ventures or strategic alliances between major international insurers and dominant local banks in high-growth regions like India, Indonesia, and Brazil.

Browse More Reports:

Global Algae Fertilizers Market

Global Construction Film Market

Global Antimicrobial Agent Market

Global Benchtop Laboratory Water Purifier Market

Asia-Pacific Feed Flavours and Sweeteners Market

Global Catenary Infrastructure Market

Global Bus Public Transport Market

Latin America Point of Care Infectious Disease Market

Global Innovation Management Market

Middle East and Africa Indium Market

Global Antibiotics Market

Global Potassium Humate Biostimulants Market

Africa MDI, TDI, Polyurethane Market

Global Dental Diode Lasers Market

Middle East and Africa Artificial Turf Market

Global Hematologic Malignancies Market

Latin America Ostomy Devices Market

Asia-Pacific Rotomolding Market

Philippines Microgrid Market

Global Automated Beverage Carton Packaging Machinery Market

Global Surgical Power Tools Market

Europe Intensive Care Unit (ICU) Ventilators Market

Global Vasodilators Market

Global Methylene Diphenyl Diisocyanate (MDI), Toluene Diisocyanate (TDI) and Polyurethane Market

Global Constrictive Pericarditis Market

Middle East and Africa q-PCR Reagents Market

Global Artificial Turf Market

Global Styrene Butadiene Latex Market

Global Digital Farming Software Market

Global Alpha Linolenic Acid Market

Global Head and Neck Cancer Drug Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com