Executive Summary

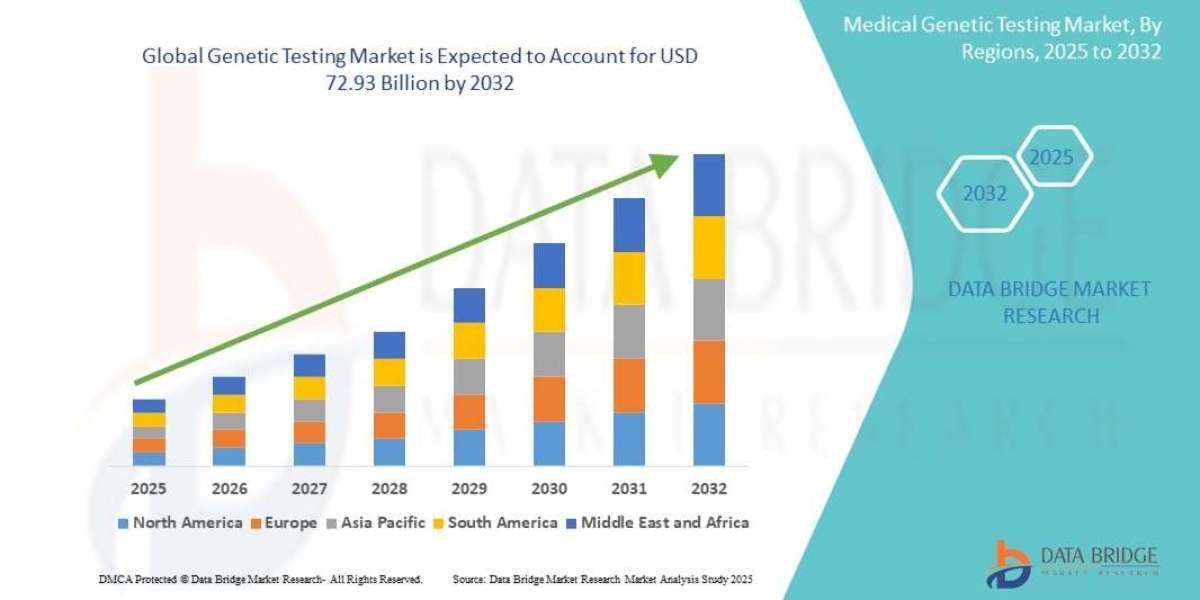

- The global genetic testing market size was valued at USD 21.49 billion in 2024 and is expected to reach USD 72.93 billion by 2032, at a CAGR of 16.5% during the forecast period

Market Overview: Defining the Genomic Landscape

Defining the Genetic Testing Market

The Genetic Testing Market involves the analysis of DNA, RNA, chromosomes, proteins, or metabolites to detect heritable or acquired genetic abnormalities.5 The market is defined by the tools, services, and applications used to extract and interpret genomic information for clinical and consumer use.

Key Segments and Dynamics

The market is highly diverse, segmented across technology, application, and product type:6

| Segmentation Category | Leading Sub-Segment (2024 Share) | Key Driver | Strategic Implication |

| By Technology | Next-Generation Sequencing (NGS) (approx. 49.3%) | Drastically reduced cost, high throughput, and capability for Whole Genome/Exome Sequencing (WGS/WES). | Continuous cost compression and integration of bioinformatics tools. |

| By Application | Oncology (approx. 36.8%) / Health & Wellness (approx. 52.3% of total genetic testing) | Critical role in cancer diagnosis, prognosis, treatment selection (companion diagnostics), and risk assessment. | Shift from tumor analysis (somatic) to hereditary risk screening (germline). |

| By Product | Consumables (approx. 60.2%) | High volume, recurring sales of reagents, kits, and buffers necessary for every test run. | Stable, recurring revenue stream dependent on test volume. |

| By Test Type | Diagnostic Testing (approx. 59.7%) | Used to confirm or rule out a suspected genetic condition. | Drives clinical and reimbursement-backed growth. |

Major Market Drivers

Advancement and Affordability of NGS: The cost of sequencing a whole human genome has plummeted from billions of dollars to near the sub-US$100 threshold, making large-scale population screening and comprehensive panels clinically feasible.7

Rise of Precision Medicine: Genetic testing is the foundation of precision oncology, pharmacogenomics (PGx), and targeted therapies, moving healthcare away from one-size-fits-all treatments.8 PGx testing, though currently a smaller segment, is projected for significant growth as it optimizes drug efficacy and minimizes adverse reactions.9

Increasing Prevalence of Genetic Disorders and Cancer: The rising global burden of hereditary cancers, rare diseases, and chronic conditions like cardiovascular and neurological disorders necessitates early and accurate genetic detection for preventative care and management.10

Consumer Empowerment (DTC Testing): The proliferation of Direct-to-Consumer (DTC) tests (e.g., 23andMe, AncestryDNA, Color Health) has increased public awareness, shifting genetic information from a strictly clinical tool to a consumer health and lifestyle offering.11

Market Size & Forecast: The Genomic Revolution

- The global genetic testing market size was valued at USD 21.49 billion in 2024 and is expected to reach USD 72.93 billion by 2032, at a CAGR of 16.5% during the forecast period

For More Information Visit https://www.databridgemarketresearch.com/reports/global-genetic-testing-market

Key Trends & Innovations ?

Innovation centers on improving the speed, accuracy, and clinical actionability of genetic data.12

1. Integration of Artificial Intelligence (AI) and Bioinformatics13

Variant Interpretation: AI and Machine Learning (ML) algorithms are crucial for analyzing the massive datasets generated by NGS, quickly identifying clinically significant genetic variants, and reducing the turnaround time for a physician's report from weeks to hours (e.g., in neonatal intensive care units).14

Predictive Diagnostics: AI models leverage genomic data alongside electronic health records (EHRs) and clinical data to enhance disease risk prediction and personalize therapeutic recommendations.15

2. Liquid Biopsy for Early Cancer Detection16

Non-Invasive Testing: Liquid Biopsy involves analyzing circulating tumor DNA (ctDNA) shed by tumors into the bloodstream. This non-invasive method is revolutionary for:

Early-stage cancer screening (minimal residual disease detection).17

Monitoring treatment response and recurrence.18

Guiding targeted therapy selection.19

3. Expansion of Pharmacogenomics (PGx)

Drug-Gene Interaction: PGx testing identifies how a patient's genetic makeup affects their response to specific drugs.20 This is expanding from specialized areas (e.g., psychiatry, cardiology) to become a standard component of prescribing protocols, driven by evidence that it reduces adverse drug reactions.

4. Direct-to-Consumer (DTC) Evolution21

Clinical Integration: DTC companies are increasingly seeking FDA authorization for health-related genetic reports (e.g., specific BRCA variants, drug metabolism genes), moving their business model from pure ancestry/wellness curiosity toward verifiable, clinically relevant information. This forces better standards for data handling and interpretation.

Employer-Sponsored Plans: A growing trend in North America is the inclusion of employer-sponsored genetic testing benefits, making clinical-grade genetic risk screening widely accessible.

Competitive Landscape: The Platform vs. Service Divide

The market is highly competitive, structured between Technology Providers (sequencing platforms) and Service Providers (labs and data interpretation).

Key Global Players

| Player Category | Key Examples | Strategic Focus | Competitive Edge |

| Sequencing Technology Providers | Illumina, Thermo Fisher Scientific, Qiagen, BGI Genomics | Dominate the equipment and consumables market. | Proprietary NGS platforms, reagent lock-in, global installed base, and low sequencing cost per base. |

| Clinical Diagnostic Labs | Quest Diagnostics, Laboratory Corporation of America (LabCorp), Myriad Genetics, Invitae | Focus on high-volume, reimbursed clinical tests (Oncology, Reproductive Health, Rare Disease). | Extensive physician networks, strong relationships with payers (reimbursement), and deep clinical validation data. |

| Direct-to-Consumer (DTC) | 23andMe, AncestryDNA, Color Health, Helix | Focus on consumer data, non-invasive sample collection, and B2B partnerships with health systems. | Massive proprietary genetic databases and high brand recognition. |

Competitive Strategies

Vertical Integration and Consolidation: Large diagnostic labs (e.g., Myriad Genetics) are acquiring smaller, specialized testing labs to expand their test menus and geographic reach.22 Sequencing platform providers are integrating software and informatics tools.

Focus on Clinical Utility (Reimbursement): Service providers heavily invest in clinical trials and peer-reviewed publications to demonstrate the value of their tests, which is critical for securing positive reimbursement coverage from government and private payers.

Data Monetization: DTC and large diagnostic companies are leveraging their vast, ethically consented genomic databases for partnerships with pharmaceutical and biotechnology firms to accelerate drug discovery and target validation.

Regional Insights: North America Dominance and APAC Acceleration

North America (NA): The dominant market globally, commanding approximately 45% of the total revenue in 2024.23

Drivers: Advanced healthcare infrastructure, high healthcare spending, strong early adoption of precision medicine, favorable reimbursement policies for complex tests, and a robust research and development ecosystem.24

Opportunity: Continued growth in PGx and liquid biopsy adoption, driven by FDA approvals.

Europe: The second-largest market, characterized by stringent data privacy regulations (GDPR) and strong, but often slower, government-led genomic initiatives.

Driver: Established public health systems incorporating newborn and cancer screening programs.

Opportunity: Focus on rare disease diagnostics and leveraging AI for data interpretation compliant with local laws.

Asia-Pacific (APAC): The fastest-growing regional market (expected to exhibit the highest CAGR).25

Drivers: Large population base, increasing disposable income, growing awareness, and significant government investments in population-scale genomic projects (e.g., India's Genome Project).26

Opportunity: Rapid adoption of affordable NGS technology and expansion of diagnostic labs to meet the rising demand for prenatal screening (NIPT) and infectious disease testing.

Challenges & Risks ?

1. Ethical, Legal, and Social Implications (ELSI)

Data Privacy and Security: The sensitive nature of genomic data necessitates rigorous security.27 Concerns over potential genetic discrimination by insurers or employers remain a significant barrier to consumer adoption, despite legal protections like the Genetic Information Nondiscrimination Act (GINA) in the U.S.28

Consent and Misinterpretation: Ensuring informed consent for the use and sharing of genetic data is complex.29 The risk of consumers misinterpreting DTC test results or making premature, non-expert medical decisions poses a public health risk.

2. Reimbursement Uncertainty and Cost

Variable Coverage: Reimbursement coverage for multigene panels and next-generation tests remains fragmented and inconsistent across payers and geographies, particularly for non-oncology or preventative applications.30 This variability creates revenue instability for service providers.

High Test Complexity: While sequencing costs are down, the overall cost of a clinical-grade test—including sample processing, bioinformatics, interpretation, and genetic counseling—remains high for complex panels.31

3. Shortage of Skilled Personnel

There is a critical global shortage of certified genetic counselors and specialized clinical bioinformaticians.32 This deficit limits the ability of the healthcare system to scale up testing, ensure proper pre- and post-test consultation, and accurately interpret complex variant data.

Opportunities & Strategic Recommendations ?

1. Strategic Recommendations for Stakeholders

| Stakeholder Group | Key Opportunity Area | Strategic Recommendation |

| Technology Providers (Illumina, Thermo Fisher) | Decentralization & Cost Erosion | Focus on developing benchtop sequencing devices and highly automated, closed-system workflows (sample-to-answer) to move NGS into smaller hospital labs, academic centers, and eventually primary care settings. |

| Clinical Diagnostic Labs (Myriad, Quest) | Clinical Utility & Payer Alignment | Invest heavily in Level 1 Evidence (Randomized Controlled Trials) to prove test utility and secure universal, positive reimbursement policies for multigene panels in oncology and PGx. |

| Fintech/Software Startups | AI-Powered Interpretation & EMR Integration | Create AI-driven clinical decision support tools that seamlessly integrate with existing Electronic Medical Records (EMRs) to provide actionable genetic insights directly at the point of care. |

| DTC Companies | Physician-Mediated Testing | Transition to a Physician-Mediated Model (e.g., Color Health), partnering directly with health systems and primary care physicians to provide clinical-grade screening, bridging the gap between consumer curiosity and clinical accountability. |

2. Market Outlook: The Convergence of Health and Wellness

The future of the Genetic Testing Market is defined by the successful convergence of high-throughput technology with clinical actionability. As the cost of sequencing approaches zero, the value shifts entirely to data interpretation, security, and clinical integration.

The market will be revolutionized by Population-Scale Screening programs (e.g., for hereditary cancer risk or cardiovascular disease) and the maturation of Liquid Biopsy into a standard screening tool. Success for industry players will depend on mastering the complexity of genomic data with AI, building unshakable consumer and clinical trust through rigorous security and validation, and demonstrating clear, measurable improvements in patient outcomes to secure long-term reimbursement.

Browse More Reports:

North America Personal Care Ingredients Market

Global FinFET Technology Market

Global Paper Dyes Market

Asia-Pacific Protein Hydrolysates Market

Global Inline Metrology Market

North America Retail Analytics Market

Global Thrombosis Drug Market

Europe Network Test Lab Automation Market

Global Perinatal Infections Market

Global Light-Emitting Diode (LED) Probing and Testing Equipment Market

Global Mobile Campaign Management Platform Market

Global Fruits and Vegetables Processing Equipment Market

Global STD Diagnostics Market

Asia-Pacific Microgrid Market

Global Fluoxetine Market

Global Food Drink Packaging Market

Global Electric Enclosure Market

Asia-Pacific Artificial Turf Market

Global Hand Wash Station Market

Global Prostate Cancer Antigen 3 (PCA3) Test Market

Asia-Pacific Hydrographic Survey Equipment Market

Global Cable Testing and Certification Market

Global Leather Handbags Market

Global Post-Bariatric Hypoglycemia Treatment Market

Europe pH Sensors Market

Global Linear Low-Density Polyethylene Market

Global Ketogenic Diet Food Market

Asia-Pacific Small Molecule Sterile Injectable Drugs Market

Global Prescriptive Analytics Market

Global Viral Transport Media Market

Middle East and Africa Composite Bearings Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com